Should I buy a house? This is the question that almost every 20- or 30-year-old must answer at some point in time. But are you getting terrible advice from parents and friends? Or do they actually know what they’re talking about? But is buying what’s best for you individually? There are so many questions to answer.

And to add to the endless questions, your parents did it, your friends and co-workers are doing it, everyone says it’s the American dream, but buying a home is a major obligation, and while there are great reasons for joining the club, there are equally important reasons for waiting.

Let’s first look at the top five reasons you should NOT buy your first home just yet:

Why You Should NOT Buy

-

Everyone is telling you to do it

Just because you just got married, graduated from college, got a great job or turned 30 doesn’t mean that you automatically need to buy a home. Individual circumstances are always different, and don’t take the home ownership path just because someone else tells you it’s time to do it.

-

You got a new job and must move

It can be stressful to suddenly find out that you have to move because of employment changes. Still, that’s not a good reason to think you have to immediately re-create your present living circumstances by buying a house. Those that quickly buy houses in an unfamiliar city sometimes find out that if they would have waited, they would have chosen a different neighborhood. Furthermore, if you think you may be transferred again within the next five years, renting may be a better option.

-

You got pre-qualified for a mortgage

Don’t borrow money just because you can. If you qualify for a mortgage today and are financially prudent, you will probably qualify in the future without much difficulty. While mortgage qualification is paramount, it should never be the only reason to purchase a home.

-

You are loaded with debt

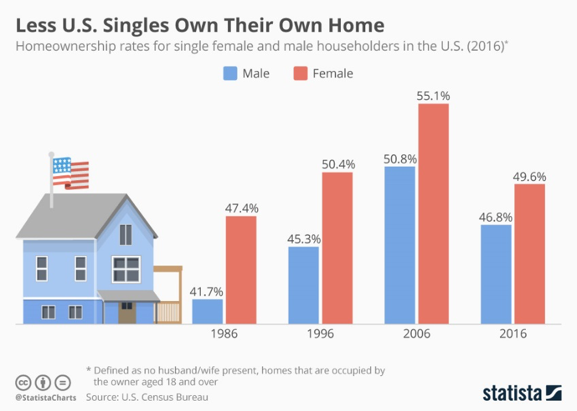

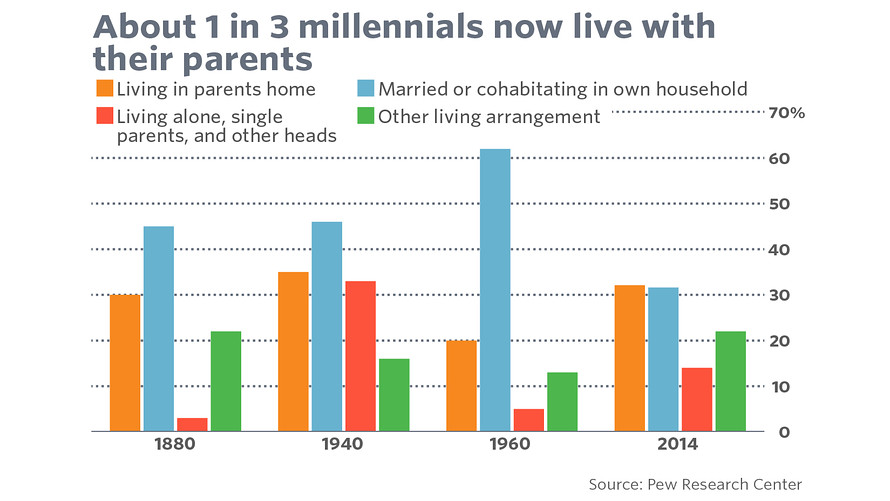

*Check out how many Millennials are NOT buying homes because of debt!

If you are just getting by and carry large credit card balances, high-payment car loans and a lot of student loan debt, you may want to make sure that you can afford a mortgage payment + taxes + insurance + maintenance + furnishings. If you can’t, then wait until you can.

-

You found a fixer-upper!

Too much HGTV may be bad for your financial health. While it’s fun to watch the Property Brothers fight through yet another renovation, reality TV sometimes skips a lot of steps and if find out you need a supporting beam and don’t have $10,000 to pay for the work, you might have been better off renting.

OK, so that takes care of the reasons not to but a home; now look at these reasons to jump into home ownership:

Why You Should Buy

-

You are finally ready

If you have saved a downpayment, your overall debt situation is good, you don’t like giving the landlord money every month with no return for you, and you really like cutting the grass, you might be ready to buy a home.

-

You want to build equity

Go to bankrate.com and calculate an amortization schedule. Even though your equity may be slow to build, a portion of every mortgage payment will go toward your principal balance. A 30 year mortgage means just that—after 30 years you will own your home and your mortgage will be gone.

-

You’re in control at work

You know when you have job security and also when things may be tenuous. If the future looks great, you have one less thing to worry about, and it may be the right time to become a homeowner.

-

Mortgage interest deduction

Even though the latest tax bill dinged the mortgage interest deduction for the rich and famous, you can still benefit if you itemize deductions. Remember however, that the standard deduction has been significantly increased, so talk to your accountant about this one. Ask about property tax deductions also.

-

We fear change

Home ownership takes a big “what if” out of the picture. As long as you make your payments, you can stay in your home. If you rent, you could be facing a different situation at lease-end, or if, for example, your apartment building is sold. Homeownership brings needed stability as it’s great knowing that you are in control.

But Wait — You Have Options!

Remember, bank mortgages aren’t the only way to finance homes. There are rent-to-own plans and better yet, MN contract for deed situations available. Alternative and non-traditional financing are two great paths to homeownership, so if you do have bad credit, large student loan balances, judgments, levies or just general bad credit, find a company like C4D that can help you.