Busting the Most Common Contract for Deed Myths

https://www.c4dcrew.com/wp-content/uploads/2018/08/CONTRACT-FOR-DEED_-PROS-AND-CONS-4.png 1000 500 Sam Radbil Sam Radbil https://secure.gravatar.com/avatar/0cd60208d9de9b4ec7236a52868375f0187854b5ee1fefa7603d0294819d3045?s=96&d=mm&r=gMN contract for deed can be an excellent way for those with less than perfect credit to finance home purchases. Particularly in Minnesota, contract for deed has been a preferred home financing method for years as many people have credit blips and issues that allow banks to quickly turn them down. Contract for deed, however, is sometimes the victim of misconceptions and broad statements that just do not apply.

It’s Not Rent-To-Own

Rent-to-own is another alternative financing method, but it can be an issue for buyers. In a Minnesota rent-to-own scenario, a property owner will offer to rent to a tenant. The property owner then agrees to put a portion of the rent aside that the tenant can put toward the eventual purchase of the home. This is not necessarily a down payment but could be a credit. For example, a property owner could offer to place $200 of the tenant’s $1500 monthly rent payment toward the purchase of the home. If the tenant made 36 on-time payments, the seller would then give the tenant credit for $7200 toward the purchase of the home. The problems with this are:

- The money doesn’t really exist after it has been paid to the landlord.

- It only is booked as a possible credit.

- If a purchase price hasn’t been predetermined, the landlord could just raise the price of the home by the amount of the credit.

- If the tenant is late on only one payment, all credits can be forfeited.

Minnesota contract for deed doesn’t work like this as we will explain below.

MN Contract for Deed is Not Predatory

In other states, rent-to-own and similar contracts for alternative financing are called executory contracts and are not liked by state courts. The reason for this is that unscrupulous property owners would find un-creditworthy victims, receive a substantial down payment, sign them to a contract that requires big monthly payments, and add clauses that forfeit the down payment if even one monthly payment is a day late. Then the property owners would evict the tenant and start the process again.

MN contract deed is different, again, as we will explain below.

It’s Not Only for Those with Bad Credit

Business owners know that even with good credit it may be difficult to purchase a home. Take the example of a restaurant owner that has paid every bill on time, but he or she may have high student loan balances, high business credit balances, too many business credit cards, multiple vehicle payments and other debt. Throw in a recent divorce, and that busy successful entrepreneur may have issues getting financing.

This is a case where MN contract for deed could help.

How MN Contract for Deed Works

- You find a Realtor

- You find a home.

- You bring the deal to C4D.

- We buy the home.

- We sell it to you using a contract for deed.

- You make all of your payments.

- You get the deed, and you are a homeowner!

If you have any questions about us or our MN contract for deed process, be sure to contact us. We make deals where others cannot, and we have an impressive list of homeowners that would still be tenants if they had not come to us.

Image source:

Image source:

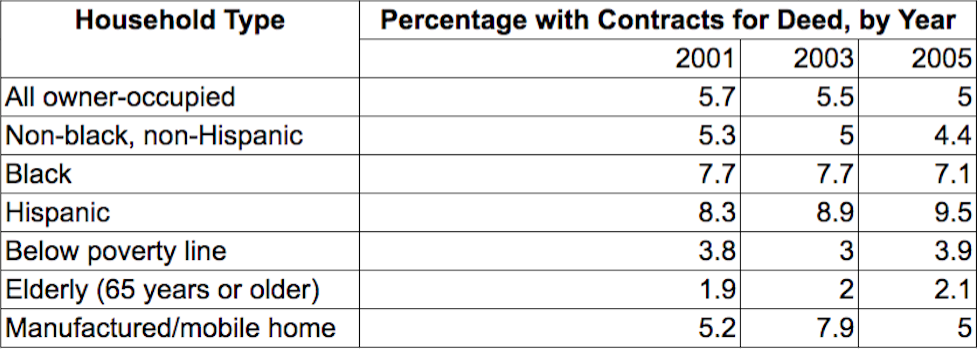

Source: American Housing Surveys 2001, 2003, 2005,

Source: American Housing Surveys 2001, 2003, 2005,