Tips to Become the Top Realtor in Your Area in 2018

https://www.c4dcrew.com/wp-content/uploads/2018/04/CONTRACT-FOR-DEED_-PROS-AND-CONS-18.png 1000 500 Sam Radbil Sam Radbil https://secure.gravatar.com/avatar/0cd60208d9de9b4ec7236a52868375f0187854b5ee1fefa7603d0294819d3045?s=96&d=mm&r=gHow to be successful in real estate? This is an extremely common question in the industry. Many real estate pros watch glamorous TV shows like Million Dollar Listing New York, House Hunters, Designed to Sell and many more. These same people would love to achieve the amount of success as many of the real estate superstars on TV. So what does it take? Is it luck? Right place and right time?

Well, there’s lots of competition in the Minnesota and Minneapolis real estate space but by following some proven business practices, you can rise to the top. From client/customer service to quality networking, let’s look at the things that can make you a top MN realtor.

How To Become Successful In Real Estate

The “t” word—transparency—has almost become a cliché, but beginning with the first Minnesota Realtor client meeting you need to be honest and forthright about expectations and costs. If the stats show that it may take 47 days to move a client’s property, don’t give then the impression that you can sell it in a week, unless, of course, you really can.

New sellers may not fully understand the commission process, and you should take some time to explain it. There may be confusion about how you share your commission and who you share it with. With median housing prices rising, the standard six percent commission can easily reach $20,000 or more, and if you have to split your commission with another broker and/or you company, your clients should understand that you don’t pocket the entire amount.

Look Like a Professional

While business casual may be sufficient in your area, showing up at a client meeting in cutoffs and a t-shirt is probably not the way to go. Then again, some will advise to dress how your clients dress. Either way, you know if you have a huge prospecting meeting that you should probably throw on your business suit and dress as professionally as possible. Projecting a professional image is critically important for real estate professionals.

Return Calls and Emails Promptly

As you undoubtedly understand, great Realtors are always working, and their clients want immediate answers. When there is a pending offer, clients on either side can get extremely hyper, and they probably won’t adhere to “normal business hours.” Have a thorough voicemail message that explains exactly when your clients can expect a return call:

“Hi – it’s Maryann. You have reached my voicemail because I’m speaking with another client or in a meeting. If you are calling before 7:00 p.m., I will return your call today. Otherwise, expect a call from me tomorrow. Please do not hesitate to text as I may be able to respond quicker that way. Also, feel free to email me at maryann@gmail.com. Regardless, I guarantee a response within 18 hours.”

This may seem basic and academic but it’s very important to do correctly.

Real Estate & Digital Media

You need a website, but a bad site with a terrible user experience and functionality may be worse than having none at all. As commonplaces.com says,

“Your website is no longer a URL at which you park the existence of your online business. It’s often the first and most powerful presentation of your business – who you are as a company, what you offer, and why your products and services are better than all the rest.”

Make sure that you find a quality developer, especially one that has experience with Realtor websites. And if you need more advice on the big picture of real estate digital media, below is a video from Million Dollar Listing star Ryan Serhant and social media influencer Gary Vaynerchuk on the state of real estate in 2018.

Social Media Presence & Brand Building

Gone are the days when a home buyer just opens up a newspaper, looks for properties, calls an agent from a phonebook and makes an offer. Buyers today are looking online more than ever. From review websites like Yelp to social media profiles like Twitter, Facebook, Instagram, LinkedIn and YouTube it is imperative that Realtors use social media to communicate with potential buyers. For example, if you worked at PlateJoy, you’d want positive platejoy reviews, right? The same goes for Realtors.

Some tips include:

- Posting photos on Instagram to generate leads

- Creating a content presence on Facebook

- Tweeting to promote listings to your audience

- Guest posting to collaborate with other local real estate pros

- Sharing your content on LinkedIn with your industry connections

- Reply to everyone and create a sense of community

Monthly Newsletter

It’s critically important for clients and potential clients to know how to find you. Start compiling an email list from day one, and send out a carefully crafted and informational newsletter. Again, you may think that this is Realtor 101, but you might be surprised at the number of your colleagues that fail to do this, start and then stop, or send out junk. A great monthly blog sent out in your newsletter will keep your name fresh.

How To Be Successful In Real Estate: Financing

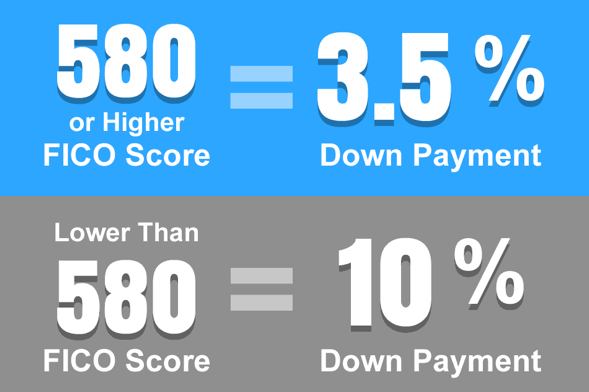

Of course, you know the deal isn’t done until funds have been wired. Savvy Realtors immediately begin building their financing network, and they know who will work hard to get marginal MN bad credit loans approved. You need to assemble your financing team, and have a go-to lender available for each particular situation, and here’s where we can help. We at C4D are MN contract for deed specialists, and every day we work with clients to make the home ownership dreams a reality. If you have difficult or even rejected financing deals, let us take a look and see if we can help. Please contact us for further information.