7 Common Mistakes First-Time Home-Buyers Make

https://www.c4dcrew.com/wp-content/uploads/2020/05/C4D-Post-Design.png 1000 500 Sam Radbil Sam Radbil https://secure.gravatar.com/avatar/0cd60208d9de9b4ec7236a52868375f0187854b5ee1fefa7603d0294819d3045?s=96&d=mm&r=gPurchasing your first home can be one of the most memorable moments in your life.

But along with this excitement can come many questions and uncertainties about making sure that the correct decisions are in place. From location to finances (and everything in between), several considerations need to be taken to ensure that buying your first house will be a fond memory to look back on.

We know you’re doing a ton of analysis and home searches, perhaps you’re diving into the Redfin vs. Realtor searches and things like that. But, first, take a look at a few common mistakes that first-time home-buyers make and how you can avoid them.

Neglecting a life insurance policy

Whereas around 85% of homeowners have homeowners insurance in the United States, another type of insurance that homeowners with a mortgage need to consider is life insurance.

While life insurance may be a task that you feel inclined to push off (as it’s harder to think about you or a partner passing during the excitement of shopping around for a new home), securing a policy can help save the financial well-being of your loved ones.

There are several different types of policies, so research which kind of plan is the most affordable option for ensuring that mortgage payments go through if there was a sudden loss of income.

Because mortgages typically extend through many years, a life insurance policy prevents passing along this debt to your partner or family. There are online life insurance resources that can help navigate how long you should plan on securing a plan for your circumstances and new homeownership, which factors will influence your rates, and which type of coverage is available.

Overlooking the importance of location

You may have found your dream home, including all the features you were looking for in your new place, along with the right price tag. But something that is just as important to remember when saying ‘yes’ to the house is also where your new home is located. Several factors make up what is considered a ‘good location,’ so spend time analyzing what can be dealbreakers or what you are willing to settle one.

For those with jobs farther from their home, make sure to factor in your daily commute and how much time you are willing to spend transporting to and from work.

Furthermore, consider those living around you. If you are seeking a quieter neighborhood, or prefer something more lively, make sure that your choice takes into account how the people around you and your surroundings will impact the satisfaction in your first home experience. Be sure not to sacrifice on location, even if it means waiting to find a better fit.

Forgetting a back-up entry plan

As mundane of a task as it may seem, many first-time home-buyers neglect to have a spare set of keys cut in case of emergency or alternative entry options after settling into their new place.

Preparing for unforeseen circumstances, in the beginning, will ensure that you will be ready for these situations before they arise. In addition to getting spare keys made, it is also a good idea to have a secure place to hide them outside of your home to avoid burglary.

If you prefer more modern or alternative technology, consider investing in a keyless door lock. Write the password information down somewhere safe and have extra batteries on hand if needed. Focusing on the security of your new home will allow you peace of mind knowing it is taken care of even when you aren’t around.

Packing unnecessary clutter

In the moving process, new homeowners should reflect on their belongings and what is actually essential to bring with them to the new house. Along with the other stresses that come along with moving into a new home, bringing unnecessary clutter can add to all the other pressures you may be dealing with.

In fact, studies have shown that the average American home consists of 300,000 items. Before committing to your moving company or making arrangements, go through your belongings and get rid of unnecessary items.

Not only can this reduce moving expenses and save you time in your unpacking process, but having less clutter can create a smoother transition and more polished home. Additionally, having a garage sale or selling unwanted items online can help diminish a few of your moving expenses.

Focusing on multiple projects

The chances are that you will want to make to your new home either after or before your move-in date—like renovations, repairs, remodels, or re-decorating. While you may feel inclined to jump into several projects at once, remember that tackling one project at a time can actually benefit how fast and efficiently you complete all your plans.

If you are looking to hire a professional for a job, search around for trusted and local people who can get the job done. Planning this out in advance will also help you gauge the amount of time needed to finish your projects— and can even be helpful to compare to which home improvement ideas you can do on your own!

Reflect on home maintenance

When selecting a new place to call home, don’t forget about the maintenance on the outside of your house. If you are looking to secure a large back yard or the property has several plants or trees that will need maintenance, consider if this is something you are willing to upkeep actively.

Examining your new home’s maintenance will also include tasks such as cleaning gutters, pest control, and roof preservation. Establishing a plan and determining how much time you are willing to spend on these responsibilities will help you set aside the necessary budget and time you will need to maintain the beauty of your new home.

Disregarding organization with finances

While you may have a vision of what you want your dream house to look like, remember when buying your first home that purchasing within your means will help your financial stability in the long run. Shifting from renters to homeownership can be an adjustment, and often time new homeowners tend to underestimate the way this lifestyle change can have an impact on the revisions you must make in dealing with your finances.

Luckily, there are professionals, like the C4D crew, that can help you navigate these tougher decisions and organization of your finances.

To gain the most of your first home-buying experience, avoid these common mistakes, and actively set yourself up for the most enjoyment in making the big move. Find confidence that you will make the right decisions, and above all, congratulations on becoming a new homeowner.

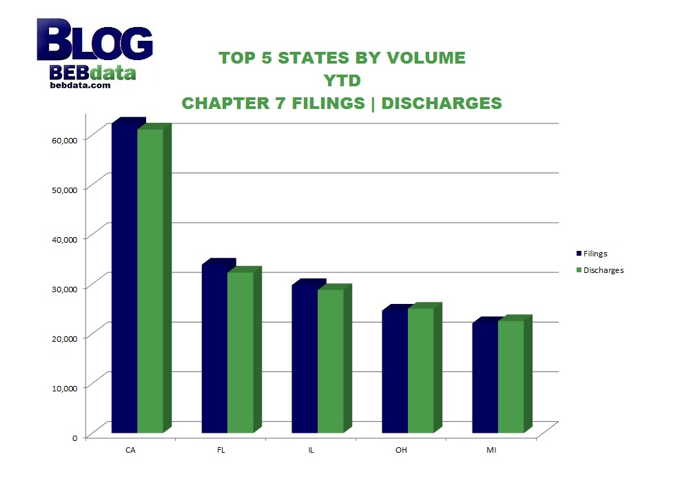

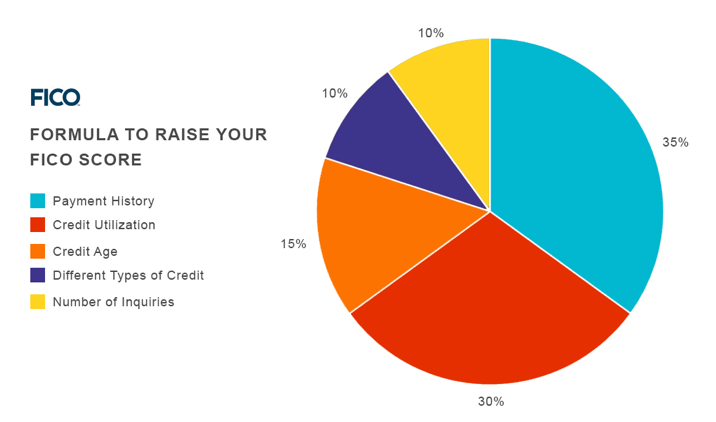

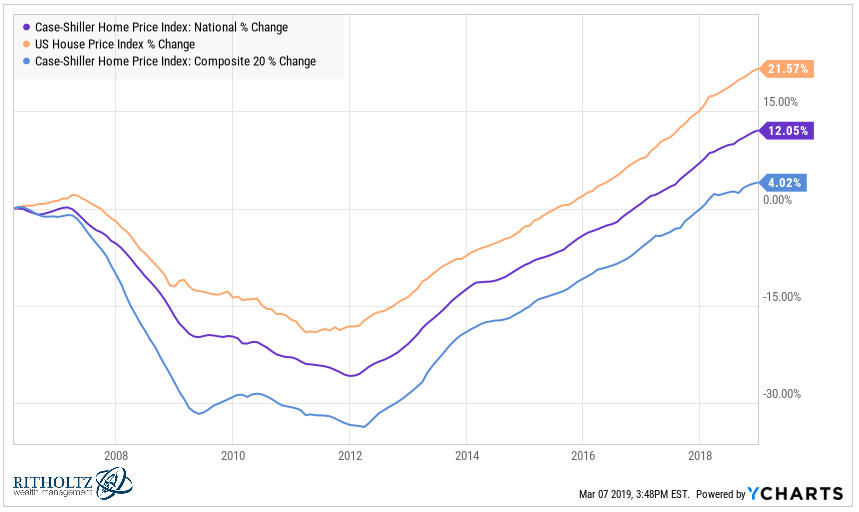

Bankruptcy – What Is It?

Bankruptcy – What Is It?